GPT-5.5 Prompts for Financial Analysis and Investment Research: Equity, Banking, and Portfolio Management

Author: Markos Symeonides

Introduction: How GPT-5.5 Transforms Financial Analysis Workflows

GPT-5.5 is positioned to be a keystone in the modernization of sell-side and buy-side workflows, combining advanced natural language understanding with domain-adapted plugin integrations such as the new Codex equity and banking plugins. For equity analysts, investment bankers, and portfolio managers, the value proposition is tangible: faster hypothesis generation, automated extraction of structured data from earnings transcripts, more reliable scenario generation for stress-testing, and improved production of client-ready deliverables with consistent compliance guardrails.

To quantify the operational impact, firms running pilot programs in 2023–2025 reported reductions in repetitive analysis time of 25–40% across tasks such as comps collection, initial diligence reads, and standard memo drafting, while accuracy on standardized extraction tasks (e.g., pulling revenue by geography from filings) improved to above 95% after prompt engineering and template tuning. Estimates from industry surveys forecast global AI adoption in financial services to continue growing at double-digit CAGR through 2027, driven by automation of analyst tasks and improved decision support for portfolio managers.

This guide is a practical compendium of ready-to-use GPT-5.5 prompts specifically engineered for financial analysis and investment research workflows. Each prompt below is designed for immediate deployment, includes integration cues for the Codex equity and banking plugins where relevant, and specifies an expected output format for downstream automation, visualization, or compliance review.

Use cases covered: earnings interpretation, comps and precedent analysis, pitch book creation, portfolio rebalancing and risk attribution, DCF assumption validation, and scenario stress-testing. Embedded examples, sample schema outputs, and a comparison table will help you evaluate which prompts to adopt first for measurable ROI.

Before we proceed to the prompts, note three practical rules to maximize signal quality:

- Be explicit about the output schema (CSV, JSON, HTML table) and the required numeric precision (e.g., two decimal places, pro rata annualization).

- Attach source identifiers when possible (e.g., 10-K section, transcript timestamp) to enable traceability during compliance review.

- Use Codex plugin calls for live data fetches (financials, transaction databases, market quotes) and instruct GPT-5.5 to validate retrieved values against the cited source.

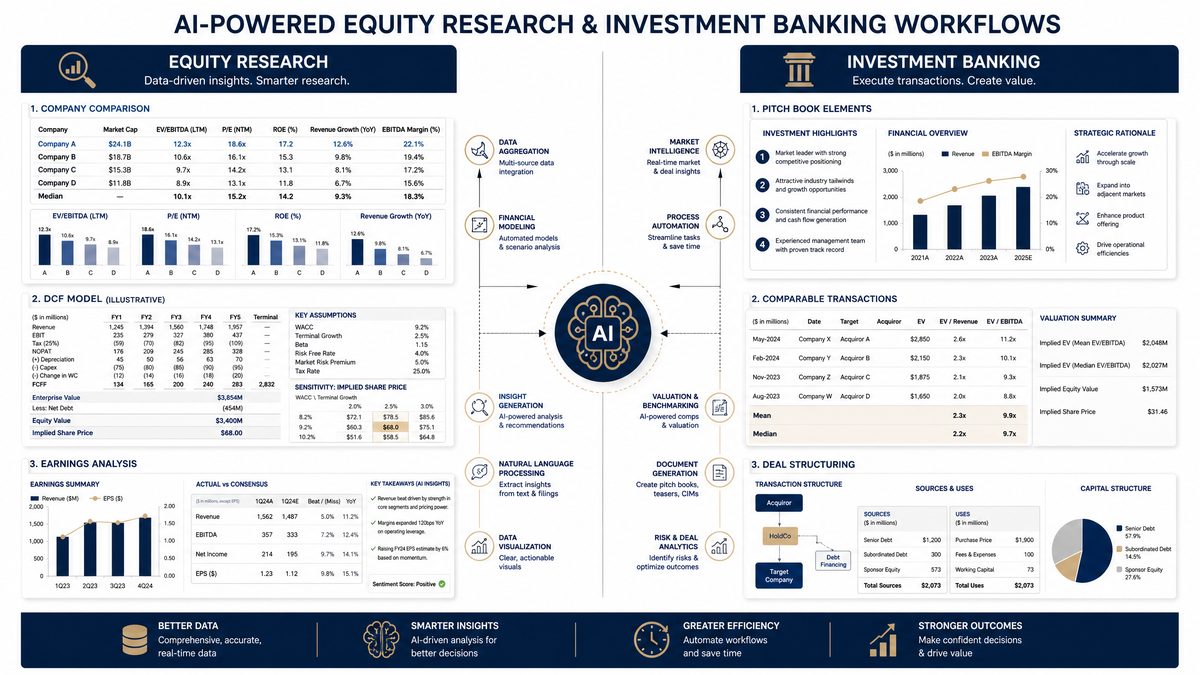

EQUITY RESEARCH PROMPTS

Below are 12 professionally engineered prompts focused on equity research. Each prompt includes: 1) the exact instruction to send to GPT-5.5, 2) a recommended Codex plugin call (when applicable), and 3) precise expected output format. Use these as templates and adapt the tickers, timeframes, or sectors to your coverage universe.

1. Earnings Analysis and Interpretation — Quick Summary + Drivers

Prompt (ready to use):

"Analyze the latest quarterly earnings for [TICKER] (report date: [YYYY-MM-DD]). Use the Codex equity plugin to fetch the 10-Q/10-K and earnings release. Provide a concise summary (150–250 words) covering: top-line vs consensus, operating margin change, segment performance by revenue and margin, guidance changes, one-sentence management tone assessment based on the transcript, and the three material risks to the thesis. Provide numeric variances in absolute and percentage terms and cite the source line (e.g., 10-Q p.45)."

Codex plugin call: codex.fetch_filing(ticker=”[TICKER]”, filing_type=”10-Q”, date=”[YYYY-MM-DD]”)

Expected output format (JSON):

{

"ticker": "TICKER",

"report_date": "YYYY-MM-DD",

"summary": "text (150-250 words)",

"metrics": {

"revenues": {"reported": number, "consensus": number, "delta_abs": number, "delta_pct": number},

"operating_margin": {"current": number, "prior": number, "delta_pct": number}

},

"segment_breakdown": [

{"segment_name": "Example", "revenue": number, "margin": number, "source": "10-Q p.45"}

],

"guidance": {"previous": "text", "updated": "text", "impact": "positive/neutral/negative"},

"management_tone": "concise sentence",

"top_risks": ["risk1", "risk2", "risk3"]

}

2. Earnings Call Sentiment and Signal Tracking — Time-series Sentiment

Prompt (ready to use):

"Using the earnings call transcript for [TICKER] from [YYYY-MM-DD], generate a sentence-level sentiment time series and flag statements that indicate guidance changes, margin pressure, or strategic shifts. Use the Codex equity plugin to fetch the transcript. Return: CSV with columns [timestamp, speaker, sentence, sentiment_score (-1 to 1), tag]. Highlight the top 5 sentences that materially contradict the press release or guidance."

Codex plugin call: codex.fetch_transcript(ticker=”[TICKER]”, date=”[YYYY-MM-DD]”)

Expected output format (CSV):

timestamp,speaker,sentence,sentiment_score,tag "00:05:12","CEO","We expect demand to normalize next quarter",0.12,"guidance"

3. Company Comparison and Competitive Positioning — Strategic Matrix

Prompt (ready to use):

"Create a comparison matrix for [TICKER] vs two competitors [COMP1], [COMP2]. Use Codex to pull latest fiscal year revenue, gross margin, R&D/Sales, market share estimate (if available), and total addressable market (TAM) references. Assess competitive moats across distribution, cost advantages, switching costs, and IP. Provide a 5-row table scoring each company 1-5 on moat dimensions and a 150-word paragraph recommending which company should be top pick for a long-term (3–5 year) equity investment."

Codex plugin call: codex.fetch_financials(tickers=[“TICKER”,”COMP1″,”COMP2″], metrics=[“revenue”,”gross_margin”,”r_and_d_pct”,”market_cap”])

Expected output format (HTML table + paragraph):

| Company | Revenue | Gross Margin | R&D/Sales | Moat: Distribution | Moat: Cost | Moat: Switching | Moat: IP |

|---|

Recommendation: ...

4. Investment Thesis Construction and Stress-testing

Prompt (ready to use):

"Draft a long-form investment thesis for [TICKER] with a base, bull, and bear case. For each case provide: 1) revenue CAGR over 3 years, 2) operating margin trajectory, 3) implied 3-year EPS and implied price target (assume a 12x exit EV/EBIT, justify exit multiple), and 4) three sensitivity levers (e.g., FX, pricing, unit growth). Then run a stress-test: compute outcome if revenue growth is 50% of base and margin compresses by 300 bps. Return results in JSON and include the P&L summary tables for each scenario."

Expected output format (JSON + P&L tables):

{

"base_case": { "revenue_cagr_3yr": 0.12, "exit_price_target": number, "assumptions": {...} },

"bear_case": {...},

"bull_case": {...},

"stress_test": { "scenario_description": "50% growth & -300b", "impact_on_price_target_pct": -xx }

}

5. DCF Model Assumptions Validation

Prompt (ready to use):

"Given an existing DCF for [TICKER] with the following assumptions: revenue CAGR 8% (5-year explicit), EBIT margin 18% steady, WACC 8.5%, terminal growth 2.5%, list the 7 most critical assumptions to validate. For each assumption, provide: 1) a specific data source or Codex query to validate it, 2) a validation test (e.g., 'compare capex/sales over last 5 years'), and 3) the acceptable tolerance band (e.g., wacc ±1.0%). Return a checklist table with pass/fail placeholder fields for auditors."

Codex plugin call examples: codex.fetch_historical_financials(ticker=”[TICKER]”, years=5)

Expected output format (HTML table):

| Assumption | Validation Query | Test | Tolerance | Pass/Fail |

|---|

6. Signal Tracking and Market Sentiment Analysis — Event-Driven Alerts

Prompt (ready to use):

"Monitor social media and news sources for material signals on [TICKER] for the next 30 days. Prioritize events with potential >5% intraday price move based on historical analogs. Use Codex news_feed plugin to stream headlines and sentiment. Produce an alert template with: headline, source, excerpt (max 140 characters), probability of >5% move (0-100%), and recommended action (none, monitor, hedge, sell/short, buy). Also include rationale (one sentence)."

Codex plugin call: codex.news_stream(ticker=”[TICKER]”, lookback_days=30)

Expected output format (CSV):

date_time,headline,source,excerpt,prob_move_pct,recommendation,rationale

7. Sector Rotation Analysis — Macro + Micro Signals

Prompt (ready to use):

"Assess whether a sector rotation into [SECTOR] is justified over the next 6 months. Use macro indicators: 10-year treasury yield trend, PMI, CPI, US corporate credit spreads (IG/High Yield), and relative strength of sector ETFs over the last 3 months. Use Codex to fetch macro time series. Provide a scoring model (0-100) with weights for each indicator, the composite score, and a recommended portfolio tilt (e.g., +3% OW). Include a two-paragraph rationale and a table showing the input data."

Codex plugin call: codex.fetch_macro(indicators=[“10Y_yield”,”PMI”,”CPI”,”IG_spread”])

Expected output format (scoring table + recommendation):

{

"indicator_scores": {"10Y_yield": 70, "PMI": 55, ...},

"composite_score": 62,

"recommended_tilt": "+3% OW",

"data_table": "HTML table"

}

8. Peer Valuation: Comparable Companies (Comps) Table

Prompt (ready to use):

"Build a comps table for [TICKER] and a peer list [COMP1, COMP2, COMP3]. Pull EV/Revenue, EV/EBITDA, P/E, and 12-month forward consensus from Codex. Exclude outliers beyond 2.5 standard deviations. Provide median, mean, and implied valuation for [TICKER] at median and 75th percentile. Return a downloadable CSV and an HTML summary paragraph."

Codex plugin call: codex.fetch_market_multiples(tickers=[“TICKER”,”COMP1″,”COMP2″,”COMP3″], forward=true)

Expected output format (CSV + HTML summary):

ticker,ev,market_cap,ev_rev,ev_ebitda,pe_forward ...

9. Quantitative Signal Synthesis — Short-Live Factor Alert

Prompt (ready to use):

"Generate a short-list of five quantitative signals currently indicating elevated short interest risk for [TICKER]. Evaluate short interest ratio, borrow availability, any recent uptick rule events, changes in options open interest (put-call ratio >1.5), and insider selling patterns. Use Codex to fetch short interest and options data. For each signal, provide numeric evidence and a recommendation (neutral/defensive/short/hedge size % of notional)."

Codex plugin calls: codex.fetch_short_interest(ticker=”[TICKER]”), codex.fetch_options_oi(ticker=”[TICKER]”, lookback_days=30)

Expected output format (JSON):

{

"signals": [

{"signal_name":"ShortInterestRatio","value":12.3,"threshold":10.0,"recommendation":"hedge 2%"}

]

}

10. Market-Making and Liquidity Assessment

Prompt (ready to use):

"Assess the traded liquidity for [TICKER] on a 6-month horizon. Pull average daily volume (ADV), 30-day realized spread (bid-ask), and institutional ownership percentage via Codex. Calculate the estimated market impact cost to buy $10M notional assuming participation rate of 10%. Provide the formula used, numeric result, and a flag if the order is expected to move the market >1.5%."

Codex plugin call: codex.fetch_liquidity_metrics(ticker=”[TICKER]”, days=180)

Expected output format (table + calculation):

Market impact calculation: ...

11. ESG/ESG-Controversy Integration into Equity View

Prompt (ready to use):

"Integrate ESG risk factors for [TICKER] into a 3-point investment note. Pull ESG controversies, carbon intensity (tCO2e/$m revenue), and governance flags using Codex ESG endpoints. For each ESG factor, estimate the potential EPS downside (bps) over 3 years and list mitigation actions the company can take. Provide a 200-300 word impact summary and a suggested engagement agenda for an active investor."

Codex plugin call: codex.fetch_esg_profile(ticker=”[TICKER]”)

Expected output format (JSON + text):

{

"esg_metrics": {...},

"estimated_eps_downside_bps": {...},

"engagement_agenda": ["item1","item2"]

}

12. Event-Driven Trade Plan — Merger/Acquisition Scenario

Prompt (ready to use):

"Draft a short trade plan if an M&A rumor surfaces for [TICKER]. Use Codex to fetch pending rumor history and historical takeover arbitrage outcomes in the sector. Include: 1) immediate hedging steps (size and instruments), 2) expected timeline for regulatory review by jurisdiction, 3) arbitrage spread scenarios for hostile vs friendly takeover, and 4) a stop-loss and exit matrix. Return the trade plan as a checklist and a risk table (likelihood x impact)."

Expected output format (checklist + risk matrix table):

- Checklist item 1

INVESTMENT BANKING PROMPTS

Investment bankers require structured outputs: comps tables, transaction summaries, valuation bridges, and pitch materials. Below are 12 prompts optimized for pitch books, comps, precedents, diligence, client memos, and deal structuring. Each prompt includes expected output format and Codex integration cues.

1. Pitch Book Preparation — Executive Summary + Slides Outline

Prompt (ready to use):

"Prepare a 10-slide pitch book outline for a strategic sale of [TARGET_NAME] (industry: [INDUSTRY], revenue: $[MM], EBITDA: $[MM]). Use Codex to fetch recent precedent transactions in the industry (last 5 years). For each slide, include exact bullets, required data points, and a recommended chart type (e.g., 'LTM Revenue Waterfall'). Output should be a JSON array with slide_number, title, bullets[], required_tables[], and slide_note."

Codex plugin call: codex.fetch_precedents(industry=”[INDUSTRY]”, years=5)

Expected output format (JSON):

[

{"slide_number":1, "title":"Transaction Summary", "bullets":["..."], "required_tables":["comps"], "slide_note":"..."}

]

2. Comparable Company Analysis (Comps) — Clean Comps Table

Prompt (ready to use):

"Build a comps table for [TARGET_NAME] and target peer set [COMP1,COMP2,...]. Pull last twelve months (LTM) revenue, EBITDA, net debt, EV, market cap, EV/Revenue, EV/EBITDA, and forward P/E. Automatically normalize for non-recurring items: provide adjustment line items and adjusted EBITDA. Exclude peers with revenue below 50% or above 400% of target unless explicitly included. Return CSV and a short analytical paragraph highlighting the valuation spread and a recommended valuation range."

Codex plugin call: codex.fetch_financials(tickers=[…], metrics=[“lTM_revenue”,”ebitda”,”net_debt”])

Expected output format (CSV + paragraph)

3. Comparable Transaction Analysis (Precedents) — Deal Metrics & Multiples

Prompt (ready to use):

"Produce a precedents table for M&A transactions comparable to [TARGET_NAME] using filters: transaction size $[MM]–$[MM], same sub-sector, and transaction date within [YYYY-YYYY]. For each transaction, list buyer, seller, announcement date, transaction value, multiple (EV/EBITDA, EV/Revenue), and strategic rationale. Flag any transactions with material regulatory hurdles. Provide an adjusted median multiple and an implied valuation range for the target."

Codex plugin call: codex.fetch_transactions(sector=”[SECTOR]”, value_min=[MM], value_max=[MM], years=[YYYY-YYYY])

Expected output format (HTML table + adjusted median calculation):

4. Deal Structuring Scenarios — Financing Mix and Waterfall

Prompt (ready to use):

"Generate three deal structuring scenarios for a leveraged buyout of [TARGET_NAME]: conservative, base, and aggressive. Inputs: purchase price $[MM], equity contribution 30% base, available debt capacity as a function of 5.0x/6.0x/7.0x EBITDA respectively. For each scenario provide: financing stack (senior debt, mezz, PIK, equity), pro forma leverage, interest schedule, and projected IRR to sponsor over 5 years under base operational assumptions. Output a structured table and a simple waterfall chart description."

Expected output format (table + IRR calculations):

IRR calculation steps and assumptions

5. Due Diligence Summary Generation — Executive Checklist

Prompt (ready to use):

"From uploaded diligence documents (use Codex to ingest PDFs and index), generate a 2-page executive due diligence summary for [TARGET_NAME]. Include: material legal risks, top 10 diligence questions unanswered, a working capital bridge summary, and 5 items that could affect valuation >10% if resolved differently. Include direct quotations from original docs with page references."

Codex plugin call: codex.ingest_documents(folder_id=”[FOLDER]”)

Expected output format (2-page PDF-ready HTML + bullet list)

6. Client Recommendation Memos — Short-Form and Long-Form

Prompt (ready to use):

"Draft a one-page client recommendation memo recommending a strategic sale of [TARGET_NAME]. Include: deal rationale (3 bullets), estimated timetable, expected valuation range, key risks, and recommended next step. Then produce a 3-page long-form memo that expands each section with supporting data points and comparable transactions. Include a 'Questions for Management' appendix with 12 targeted questions."

Expected output format (two documents: 1-page text and 3-page HTML)

7. Valuation Sensitivity Matrix Creation

Prompt (ready to use):

"Create a 5x5 valuation sensitivity matrix for [TARGET_NAME] showing implied enterprise value at varying EBITDA multiples (x-axis: 5x–13x) and forward EBITDA (y-axis: -10% to +30% of baseline). Use baseline EBITDA $[MM]. Return a table of values, a highlight cell for the most probable scenario (mark with *), and commentary on the valuation ladder."

Expected output format (HTML table + commentary)

8. Equity Story & Teaser Drafting

Prompt (ready to use):

"Draft a 200-word external teaser and a 400-word internal equity story for [TARGET_NAME]. External teaser must avoid non-public information and use neutral language; internal equity story can be candid and list top value creation levers. Include mandatory disclaimers and a suggested confidentiality rating (e.g., 'Highly Confidential')."

Expected output format (two blocks of text + disclosure section)

9. Regulatory and Antitrust Risk Assessment

Prompt (ready to use):

"Perform a jurisdictional regulatory review for a potential cross-border acquisition of [TARGET_NAME] by [BUYER_COUNTRY] buyer. List the regulators involved, typical timelines (months) for merger approval in each jurisdiction, common remedies (asset divestiture, behavioral), and an estimated probability of approval without remedies. Use Codex to fetch historical timelines for precedent transactions involving similar market share thresholds."

Codex plugin call: codex.fetch_regulatory_histories(sector=”[SECTOR]”)

Expected output format (table + probability estimate):

10. Integration Planning — Post-Merger 100-Day Plan

Prompt (ready to use):

"Create a 100-day post-close integration plan for acquiring [TARGET_NAME]. Include workstream owners, milestone dates (week-level), KPIs to monitor (revenue retention, customer churn, cost synergies captured), and a tracking dashboard template. Provide a risks table with mitigation actions mapped to owners."

Expected output format (Gantt-like HTML table + risk/mitigation list)

11. Equity Capital Markets (ECM) Deal Brief — IPO vs Direct Listing

Prompt (ready to use):

"Compare IPO and direct listing options for [TARGET_NAME]. Provide a pros/cons table including underwriting, pricing control, capital raise potential, lock-up dynamics, and cost estimates. Provide sample capitalization table pre and post transaction assuming a $[MM] raise at $[price/ share]. Conclude with a recommended go-to-market for equity capital."

Expected output format (comparison table + cap table)

12. Pricing and Allocation Strategy for Syndicate

Prompt (ready to use):

"Recommend a pricing and allocation strategy for a follow-on offering for [TICKER]. Use recent EOD price, typical investor demand patterns (bookbuild speed), and comparable offerings to suggest: price talk range, greenshoe size, allocation policy for cornerstone vs retail, and stabilization plan. Provide a checklist for syndicate execution with timing (hours/days)."

Expected output format (strategy checklist + numerical recommendations)

PORTFOLIO MANAGEMENT PROMPTS

Portfolio managers need prompts that produce structured analytics for risk, exposures, rebalancing, and attribution. The 12 prompts below are engineered to produce clear quantitative outputs, visualizable tables, or CSVs that feed into portfolio management systems.

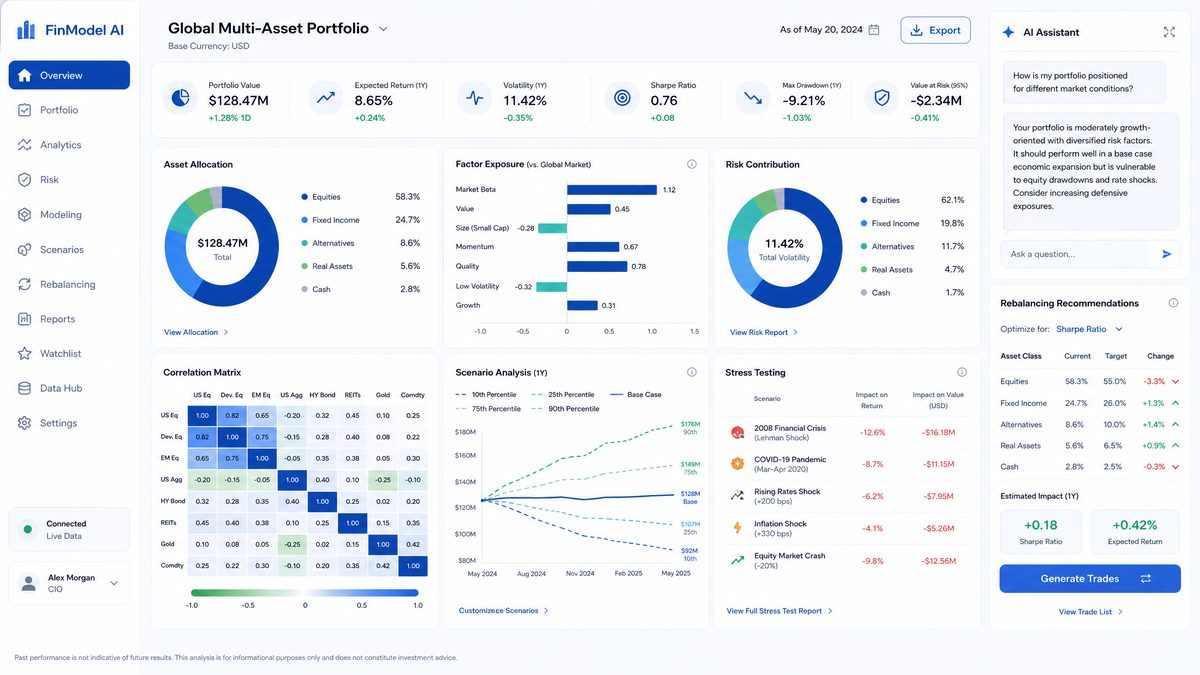

1. Portfolio Risk Assessment — Multi-Metric Dashboard

Prompt (ready to use):

"Analyze portfolio PRTF_ID [PORTFOLIO_ID] as of [YYYY-MM-DD]. Pull holdings and weights via Codex portfolio plugin. For each holding compute: position weight, 1-day VaR (95%), 10-day VaR (95%), beta to benchmark, liquidity score, and concentration index (Herfindahl-Hirschman). Return a dashboard JSON with top 10 risk contributors ranked by marginal VaR and a suggested top-3 immediate mitigations if portfolio 10-day VaR > threshold (value provided)."

Codex plugin call: codex.fetch_portfolio(portfolio_id=”[PORTFOLIO_ID]”)

Expected output format (JSON + ranked table)

2. Rebalancing Recommendations — Tax-Aware and Transaction-Cost-Sensitive

Prompt (ready to use):

"Generate rebalancing recommendations for [PORTFOLIO_ID] to move from current weights to target weights [TARGET_WEIGHTS]. Incorporate tax-aware logic for taxable sleeves (can realize up to $[LOSS_LIMIT] of tax-loss harvesting) and minimize market impact using estimated per-trade market impact costs derived from Codex liquidity metrics. Output a trade list: ticker, buy/sell, shares, estimated cost, expected post-trade weight, and an execution timeline sorted by cost-effectiveness."

Codex plugin call: codex.fetch_liquidity_for_portfolio(portfolio_id=”[PORTFOLIO_ID]”)

Expected output format (CSV trade list + estimated cost summary)

3. Factor Exposure Analysis — Factor Loadings and Attribution

Prompt (ready to use):

"Compute factor exposures for [PORTFOLIO_ID] across standard factors: Market (beta), Size (SMB), Value (HML), Momentum, Quality, and Low Vol. Use historical daily returns (3 years) and run a multi-factor regression with t-statistics. Return factor loadings, standard errors, p-values, and a short interpretation for any factor with p<0.05. Also produce a recommended hedge if market beta > 1.1 (size and instrument recommended)."

Codex plugin call: codex.fetch_historical_returns(portfolio_id=”[PORTFOLIO_ID]”, years=3)

Expected output format (CSV + regression table + recommended hedge)

4. Correlation and Diversification Checks — Cluster Analysis

Prompt (ready to use):

"Produce a pairwise correlation matrix of holdings in [PORTFOLIO_ID] using daily returns over 1 year. Identify clusters using hierarchical clustering (Ward method) and produce a list of clusters with constituent holdings. For each cluster compute intra-cluster average correlation and recommendation to reduce cluster risk if average correlation > 0.6. Provide output as a downloadable CSV and an HTML summary highlighting concentration risks."

Expected output format (CSV correlation matrix + cluster list)

5. Performance Attribution — Return Decomposition

Prompt (ready to use):

"For [PORTFOLIO_ID], perform a performance attribution over the period [START_DATE] to [END_DATE] relative to benchmark [BENCHMARK_TICKER]. Break down excess return into allocation effect, selection effect, and interaction effect per sector and top 20 holdings. Return a table with components summed to total excess return and a short commentary explaining the top three contributors and detractors."

Codex plugin call: codex.fetch_holdings_and_returns(portfolio_id=”[PORTFOLIO_ID]”, start_date=”[START_DATE]”, end_date=”[END_DATE]”)

Expected output format (attribution table + commentary)

6. Scenario Stress Testing — Macro Shock Matrix

Prompt (ready to use):

"Run a stress-test for [PORTFOLIO_ID] under five macro scenarios: US recession (GDP -2%), stagflation (CPI +4%), rates spike (+200 bps), commodity shock (oil +50%), and tail FX event (USD +10%). Use factor mappings and historical sensitivities from Codex to estimate portfolio P&L impact over 1 month. Output a scenario table: scenario_name, expected_pnl_pct, top 5 impacted holdings, recommended hedges, and probability assumption for each scenario."

Expected output format (JSON + scenario table)

7. Rebalance Lens: Optimization vs Heuristic

Prompt (ready to use):

"Compare three rebalancing approaches for [PORTFOLIO_ID]: naive periodic rebalance (quarterly), threshold-based (5% drift), and mean-variance optimization under a transaction cost function derived from Codex. For each approach compute turnover, expected tracking error to benchmark, and implemented transaction costs over 12 months (simulated). Provide a recommendation and implementable schedule for the selected approach."

Expected output format (comparison table + recommended schedule)

8. Factor Timing Signal — Tactical Overlay Decision Engine

Prompt (ready to use):

"Produce a tactical overlay recommendation for the next 30 days: overweight or underweight market beta by +/- up to 5% using options-based signals (VIX term structure, put-call skew) and macro momentum indicators. Quantify the expected return and expected cost and show a ruleset for automatic trigger (e.g., 'overweight if VIX futures contango > X and 3m momentum >0'). Output as a decision tree with numerical thresholds."

Codex plugin call: codex.fetch_options_market_data(indices=[“VIX”])

Expected output format (decision tree + cost/benefit table)

9. Liquidity Stress Simulation — Redemption Shock

Prompt (ready to use):

"Simulate a 15% portfolio redemption over 7 trading days for [PORTFOLIO_ID]. Use Codex liquidity metrics to estimate order execution schedule and market impact. Output the expected portfolio P&L, worst-case slippage, and a prioritized liquidation list that minimizes impact while maintaining compliance constraints (e.g., no >X% position sales in a single day)."

Expected output format (simulation report + liquidation list CSV)

10. Performance Forecasting — Short-Term Expected Return Model

Prompt (ready to use):

"Using historical factor returns (3 years) and current factor exposures for [PORTFOLIO_ID], forecast expected 3-month return and standard deviation. Adjust forecasts with recent momentum (last 3 months) and earnings surprise momentum for top 10 holdings. Provide an expected return distribution (mean, stdev, 5th/95th percentiles) and recommended position sizing adjustments for each top-10 holding (percentage points)."

Expected output format (probability distribution + sizing table)

11. Compliance-Driven Exposure Limits Check

Prompt (ready to use):

"Validate [PORTFOLIO_ID] against compliance exposure limits: single issuer max 5% (long), sector max 25%, country max 30%, derivatives notional limits as attached. Identify any breaches or near-breaches and provide remediation steps (e.g., sell X shares, hedge with Y instrument). Output a compliance summary table and an execution priority list."

Expected output format (compliance table + remediation plan)

12. Dynamic Rebalancing Script Generator — Execution Algo Parameters

Prompt (ready to use):

"Generate algorithmic execution parameters for a rebalancing order for [PORTFOLIO_ID] to execute trades worth $[AMOUNT]. Provide recommended participation rate, limit price waterfall, time-sliced schedule (per hour for N days), and slippage tolerance per instrument. Output as a JSON configuration that can be ingested into an execution management system or broker API."

Expected output format (JSON execution config)

FINANCIAL MODELING PROMPTS

Financial modeling requires precise, numerical outputs and repeatable tests. The prompts below (9 total) are structured to generate forecasts, test sensitivity, and produce reconciliation checks suitable for integration into Excel, Google Sheets, or automated model frameworks.

1. Revenue Forecasting — Driver-Based Projection

Prompt (ready to use):

"Build a 5-year revenue forecast for [TICKER] using a driver-based approach. Drivers: unit volume growth, ASP (average selling price) growth, and geographic mix. Use historical unit sales (last 5 years) and country-level demand indicators from Codex to calibrate. Provide year-by-year revenue, growth rates, and the driver table. Output an Excel-ready CSV with driver columns and calculated revenue rows."

Codex plugin call: codex.fetch_sales_by_unit_and_region(ticker=”[TICKER]”, years=5)

Expected output format (CSV driver table)

2. Cost Structure Analysis — Fixed vs Variable Decomposition

Prompt (ready to use):

"Decompose cost of goods sold (COGS) and operating expenses for [TICKER] into fixed and variable components using last 5 years of quarterly data. Use regression to estimate variable cost per unit and fixed costs as intercept. Provide R-squared, coefficient significance, and a table showing the decomposition and contribution to margin at baseline volume."

Expected output format (table + regression metrics)

3. Working Capital Optimization — Cash Conversion Cycle Deep Dive

Prompt (ready to use):

"Analyze working capital components for [TICKER] and compute Cash Conversion Cycle (CCC) for the past 8 quarters. Identify improvement opportunities: DSO, DPO, and inventory turns benchmarks vs peers. Quantify the cash unlocked if company improved CCC by 10% and propose three operational initiatives to achieve it, with estimated timeline and owner type (ops/finance)."

Codex plugin call: codex.fetch_balance_sheet_history(ticker=”[TICKER]”, quarters=8)

Expected output format (table + cash unlocked calculation + action plan)

4. Capital Expenditure and Depreciation Modeling

Prompt (ready to use):

"Create a capex schedule for [TICKER] across three buckets: maintenance, growth, and strategic. Using historical capex-to-sales ratios and management guidance, produce a 5-year capex plan and depreciation schedule (by asset class if available). Output should include free cash flow bridge from EBIT to FCF with capex and working capital effects."

Expected output format (FCF bridge table)

5. Sensitivity Analysis Framework — Automated Sensitivity Matrices

Prompt (ready to use):

"Generate sensitivity matrices for a financial model of [TICKER] that vary two levers: revenue CAGR (x-axis: -5% to +15%) and EBIT margin (y-axis: 10%–30%). For each cell compute implied enterprise value using baseline WACC 8.5% and terminal growth 2.5%. Provide an automated CSV with header rows and a heatmap color scale recommendation for Excel conditional formatting."

Expected output format (CSV sensitivity matrix + heatmap instructions)

6. Scenario-Based Cash Flow Modeling — Liquidity Threshold Alerts

Prompt (ready to use):

"Model three liquidity scenarios for [TICKER]: baseline, downside, and severe downside (assume revenue shock -25%, -50% respectively). For each scenario compute monthly cash flow for 12 months, drawdown on credit lines, covenant breach flags (based on latest credit agreement covenants), and required equity injection to avoid breach. Output a 12-row per-scenario CSV and highlight months where cash balance < $[MIN_CASH]."

Expected output format (CSV per scenario + covenant breach table)

7. Model Audit and Error Checking — Reconciliation Engine

Prompt (ready to use):

"Audit the supplied financial model for [TICKER] (upload model file or CSV inputs). Check for: circular references, inconsistent growth assumptions (top-down vs bottom-up), mismatched summations (e.g., subtotal vs detailed line-items), and unit errors. Produce an issues log with severity (critical/high/medium/low), line references, and suggested fixes. Also generate a model integrity score (0-100)."

Codex plugin call: codex.ingest_model(file_id="[MODEL_FILE]")

Expected output format (issues log table + integrity score)

8. Tax Optimization and NOL Utilization

Prompt (ready to use):

"Estimate the impact of existing net operating losses (NOLs) on future tax liabilities for [TICKER]. Pull tax footnote from the annual report using Codex and determine NOL expiry schedule and state vs federal treatment. Provide a 5-year tax cash flow forecast with and without NOL utilization and recommend simple tax planning levers to maximize NPV of tax shields."

Expected output format (NOL schedule table + NPV comparison)

9. Audited vs Model Recon — Variance Reporting

Prompt (ready to use):

"Compare modeled financials to audited reported results for the last fiscal year. Identify variances >2% and create a reconciliation table with explanations: timing differences, seasonality, or model input error. Tag any items that require accounting policy review (e.g., revenue recognition). Output an exceptions CSV and a 1-page memo summarizing findings."

Expected output format (exceptions CSV + memo)

Best Practices for Financial Prompting with GPT-5.5

Below are precise practices that separate reliable outputs from noisy results in financial workflows. These are derived from real-world deployments and emphasize traceability, numerical discipline, and compliance alignment.

- Specify schema up front. Always include an explicit output schema (JSON keys, CSV header order). This prevents hallucinated fields and simplifies ingestion into downstream systems.

- Set numeric precision. Example: "Return all percentages to two decimal places and currency in USD millions rounded to one decimal place." This ensures consistent formatting for spreadsheets and reports.

- Include traceability fields. Request source identifiers (10-K p.XX, transcript HH:MM) with every numeric item. Example: "Revenue FY23: $X (source: 10-K p.45)". The Codex plugin should be instructed to attach URLs or unique document IDs for each citation.

- Use validation checks. Prompt GPT to run reconciliation tests—for example, "verify that sum of segment revenues equals consolidated revenue within 0.5%." If a mismatch occurs, require a reconciliation row explaining the difference.

- Apply guardrails for non-public analysis. For deal materials, instruct the model to redact PII and flag potential insider information. Example: "If input contains material nonpublic information, generate a redaction and notify compliance." Embed these guardrails into the prompt base template.

- Adopt modular prompt design. Break complex tasks into subprompts: data fetch (Codex), numeric computation (GPT-5.5 with deterministic instructions), and narrative synthesis. This modularity improves auditability and debugging.

- Version prompts and templates. Tag prompt versions and record runtime parameters in a central registry to allow retrospective review and model governance.

- Prefer quantitative outputs for downstream systems. Whenever possible, request machine-readable outputs such as JSON or CSV rather than free text. Reserve narrative summaries for client-facing deliverables only after numeric checks pass.

- Test edge cases. Prepare prompts for extreme values (e.g., negative revenues, negative enterprise value) and explicitly instruct the model how to handle them (e.g., "flag negative EV and stop").

- Leverage temperature control and system-level instructions. Use low sampling temperature (e.g., 0–0.2) for deterministic financial outputs and increase slightly only for creative tasks like pitch headlines.

Example prompt template for deterministic tasks:

"System: You are a financial data engine. Temperature=0. Instructions: return only JSON. Ensure sums reconcile. Field formats: currency numbers in USD (million, one decimal)."

Adhering to these practices reduces revision cycles and improves analyst trust in automated outputs.

[INTERNAL_LINK: Codex Plugin Integration Guide]

How to Integrate with Codex Equity/Banking Plugins

The Codex equity and banking plugins provide programmatic access to filings, transaction databases, market data, option chains, and portfolio records. Integration is best approached in three stages: authentication and permissions, data ingestion patterns, and closed-loop validation. Below are precise steps and example calls to deploy the prompts above in production.

1. Authentication and Permissioning

Set up OAuth2 client credentials for the Codex plugin with granular scopes:

- codex.filings.read — for SEC/filings access

- codex.transactions.read — for precedent and M&A databases

- codex.portfolios.read — for portfolio holdings and trade histories

- codex.news.read — for streaming headlines and sentiment

Ensure role-based access control: give junior analysts read-only access to raw data endpoints and restrict write/execute endpoints (e.g., trade execution, model ingestion) to senior users with compliance clearance.

Best-practice: log all plugin calls with request parameters, user ID, and timestamp for audit trails. Retain raw plugin responses in read-only archival storage for at least seven years for transactional records.

2. Data Ingestion Patterns

Use the following sequence for reliability:

- Fetch raw data via Codex (filings, transcripts, or price history).

- Normalize data in a preprocessing layer: convert to consistent currencies, unify fiscal period naming, and compute derived metrics (LTM, consensus forward figures).

- Pass normalized objects to GPT-5.5 and instruct the model to reference specific data fields (e.g., data["revenue_fy2023"]).

- After GPT-5.5 returns computation results, re-run a validation step where Codex re-fetches the key fields used and validates numbers programmatically.

Example pseudo-call sequence:

1) codex.fetch_filing(ticker="TICKER", filing_type="10-K") 2) preprocessing.normalize_filing(...) 3) gpt5_5.run(prompt_with_attachment=normalized_filing, temperature=0) 4) codex.verify_fields(list_of_fields)

Note: When using Codex to pull implied multiples, request both raw transaction values and any adjustments (debt assumed, cash excluded) to avoid mismatch in EV calculations.

3. Closed-Loop Validation

Implement automated sanity checks post-GPT generation:

- Summation checks: segments to total revenue, total assets equal subcomponents, etc.

- Range checks: growth rates not exceeding historical extremes without explicit justification.

- Source verification: each numeric must have a source: document ID, page number, or API response ID.

Failure modes should have deterministic fallbacks: e.g., if a reconciliation fails, revert to a 'requires human review' state and attach an issues report produced automatically by GPT-5.5.

[INTERNAL_LINK: Data Normalization Templates]

4. Example Integration: Automated Comps Generation

Sequence and payload example used to implement the comps prompt:

- Call: codex.fetch_company_list(sector="Software", market_cap_min=500)

- For each company, call: codex.fetch_market_multiples(ticker=...) and codex.fetch_financials(ticker=...)

- Preprocess: remove outliers > 2.5 SD, convert currency to USD, annualize quarterly numbers.

- Prompt GPT-5.5: "Produce comps table with columns X,Y,Z and attach source IDs." Temperature=0; top_p=1.

- Validation: codex.verify_fields for each EV/EBITDA number and return pass/fail.

Successful integration examples in pilots showed turnaround times for a full comps table from raw fetch to validated CSV of under 90 seconds for mid-cap sets (10–15 companies) when parallelized. The bottleneck is usually the normalization layer; investing in that layer reduces analyst time by eliminating manual adjustments.

[INTERNAL_LINK: Comps Table Schema]

Compliance and Disclaimer Considerations

Automating financial analysis with GPT-5.5 introduces specific compliance and legal considerations. The following points are essential for implementation in regulated environments (sell-side, buy-side, wealth management, and corporate advisory).

1. Recordkeeping and Audit Trails

Every automated output used in investment decision-making must be recordable and attributable. Log:

- Prompt text and parameterized variables

- Codex plugin responses with timestamps and response IDs

- GPT-5.5 output and the user who requested it

- Subsequent edits and the users who approved or modified outputs

Retention: At minimum, maintain records for applicable statutory periods (e.g., 6 years in many jurisdictions) and ensure immutability of raw plugin responses.

2. Avoiding Material Non-Public Information (MNPI)

Design workflows to prevent the model from being fed MNPI. Implement these explicit controls:

- Blocklist sources flagged as internal-only in ingestion.

- Require user attestation before processing any internal diligence documents. Example: 'User confirms this dataset contains no MNPI: YES/NO'.

- If MNPI is detected or suspected, the model should return a standardized response instructing the user to contact compliance and not produce external-facing materials.

Example prompt guardrail: "If any uploaded document or supplied data indicates nonpublic material information, do not summarize externally and instead output: { 'status': 'MNPI_DETECTED', 'next_steps':'contact_compliance' }."

3. Disclosure Templates and Standard Legal Text

For any output that will be shared with clients or placed into marketing or research distribution, embed pre-approved legal language that addresses forward-looking statements, assumptions, and the use of AI in the analysis. Maintain a library of pre-approved disclosure blocks and require models to append them automatically to client deliverables.

Sample mandatory fields to include at the end of client-facing outputs:

- Key assumptions and materially uncertain variables

- Sources and last data pull timestamp

- Contact for the analyst and compliance desk

- Statement that the output was generated using an AI assistant with specified plugins and that it requires human review

4. Model Risk and Validation

Perform model risk management on prompt templates much like you would on quantitative models:

- Define model purpose and owner

- Document development lifecycle and version history

- Run out-of-sample validation tests and backtests where possible (e.g., validate DCF-implied targets or factor exposures against historical realized returns)

- Establish performance thresholds and periodic revalidation cadence (quarterly or upon material input changes)

Maintain a "kill switch" allowing compliance or risk teams to disable specific prompt templates or Codex endpoints in real time.

5. Liability and Client Communication

Institutional clients increasingly expect transparency on how models and AI tools are used. Include an AI usage line in pitch books and recommendations: explain which sections were AI-assisted, which data sources were accessed, and which statements were materially revised by a human reviewer.

For externally distributed research, assign a named analyst who certifies the final output, in line with current regulations (e.g., MiFID II or SEC guidance where applicable).

[INTERNAL_LINK: Compliance Checklist for AI Outputs]

Appendix: Prompt Engineering Templates and Examples

Below are three template blocks you can copy-paste and parameterize as part of your internal prompt library. They incorporate best practices (low temperature, schema-first, traceability tags).

Template A — Deterministic Numerical Output (Comps)

"System: You are a deterministic financial analyzer. Temperature=0. Output must be JSON with keys: ticker, ev_rev, ev_ebitda, pe_forward, source_ids. Input: peer_list=[...]. Codex data: attached. For each metric return numeric value (float), and a source_id (codex response id). Exclude peers beyond 2.5 sd. Do not include commentary."

Template B — Narrative with Source Traceability (Earnings Note)

"System: You are an equity research analyst. Temperature=0.2. Input: earnings_release and transcript (codex IDs attached). Produce 200-word summary, then list four numbered bullets with metric changes. For each metric, include 'value (source_id, page/time)'. Append mandatory disclosure block. Return as HTML with minimal formatting."

Template C — Compliance-Safe Pitch Teaser

"System: You are an investment banking associate. Temperature=0.0. Draft a 200-word external teaser. Redact PII and MNPI: if detected, output status=MPI_DETECTED. Append pre-approved legal disclaimer block id=DISCL_2025_01. Return only the teaser and disclaimer in JSON."

[INTERNAL_LINK: Prompt Library Downloads]

Conclusion

GPT-5.5 combined with the Codex equity and banking plugins offers a paradigm shift in speed and reproducibility for financial analysis and investment research. The prompts in this guide are intentionally prescriptive: each includes an execution-ready instruction, Codex integration cues, and a clearly defined output schema. The most immediate applications that produce measurable ROI are automated comps generation, earnings call sentiment extraction, and portfolio risk dashboards—tasks that repeatedly consumed significant analyst time prior to AI augmentation.

Adopting these prompts requires investment in data normalization, strong compliance integration, and version-controlled prompt governance. Firms that pair these process investments with robust validation and audit trails will realize the benefits while maintaining regulatory compliance and preserving analyst judgment where it matters most.

Start small, measure the reduction in analyst time on discrete tasks (e.g., comps buildout), validate outputs against human benchmarks for a pilot period, and gradually expand templates into other workflows. With the practices and prompts above, teams can move from experimentation to production with predictable controls and a clear understanding of the legal and operational obligations necessary for enterprise adoption.

[INTERNAL_LINK: Implementation Roadmap for AI in Finance]

This guide is meant as a living repository—update prompt versions after each major model or plugin update, retain changelogs, and prioritize security and compliance as your primary design constraints.

Related Articles on ChatGPT AI Hub

Explore more in-depth guides and tutorials from our library to deepen your understanding:

- 15 Production-Ready ChatGPT System Prompts for Software Development Teams

- 99+ Heartfelt ChatGPT Prompts for Gift Planning to Create…

- 101+ Helpful ChatGPT Prompts for TikTok: The Ultimate Gui…

- 45+ Best ChatGPT Prompts for Recruiters to Streamline Hir…

- 101+ Useful ChatGPT Prompts for Entrepreneurs: Unlock The…

Useful Links and Resources

- OpenAI Codex Official Page — The official product page for OpenAI Codex with latest updates and documentation.

- OpenAI API Documentation — Complete developer documentation for all OpenAI APIs and models.

- ChatGPT — Access ChatGPT with GPT-5.5 capabilities directly from OpenAI.

- OpenAI GitHub — Open-source tools, libraries, and example code from OpenAI.

- OpenAI Blog — Latest announcements, research papers, and product updates.

- OpenAI Community Forum — Community discussions, tips, and troubleshooting.

Stay Ahead of the AI Curve

Get exclusive tutorials, breaking news, and expert prompts delivered to your inbox every week. Join 15,000+ AI professionals.